Why Does Higher Credit Utilization Decrease Your Credit Score?

Maintaining a healthy credit score is crucial for financial stability and access to various credit options. But have you ever wondered why does higher credit utilization decrease your credit score? Credit utilization, one of the primary factors that affects your credit score, is often misunderstood. In this article, we will break down what credit utilization is, how it impacts your score, and why keeping it low is essential for maintaining a strong credit profile.

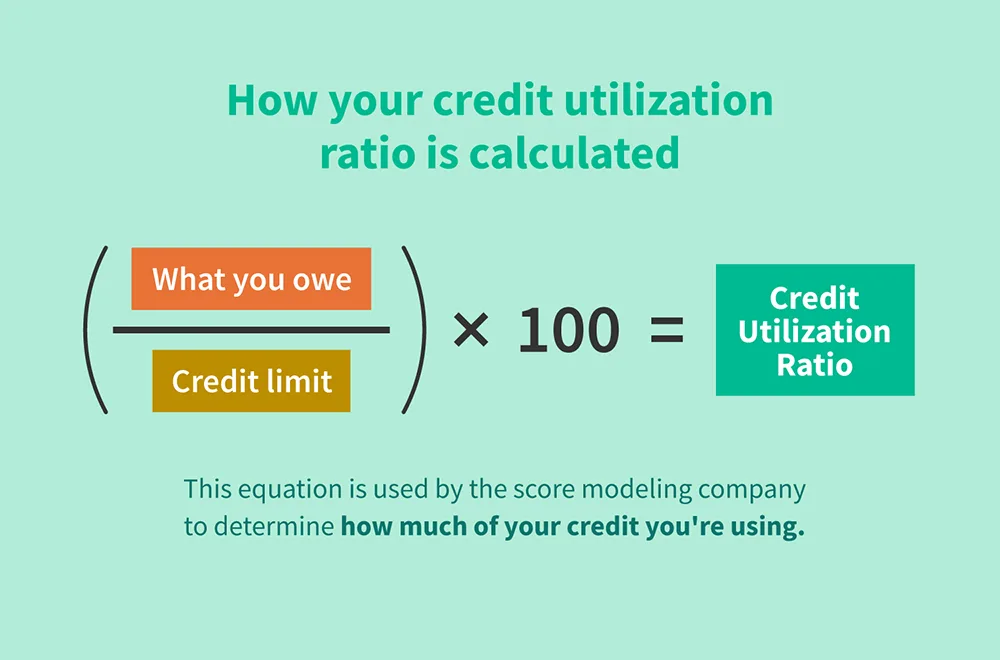

What Is Credit Utilization?

Credit utilization examines the percentage of your credit card limits that you have actually utilized Credit utilization ratio is a significant element in your credit score. Generally speaking, credit utilization is expressed as a percentage. It indicates how much of the credit that you have available to you is currently being used.

For example, if you have a total credit limit of $10,000 and a balance of $2,500, your credit utilization is 25 percent Lenders, credit bureaus and marketers all view this ratio–used to estimate how well one manages his available credit–in their own way. A lower utilization rate suggests that you are not too dependent on credit, which makes lenders happy.

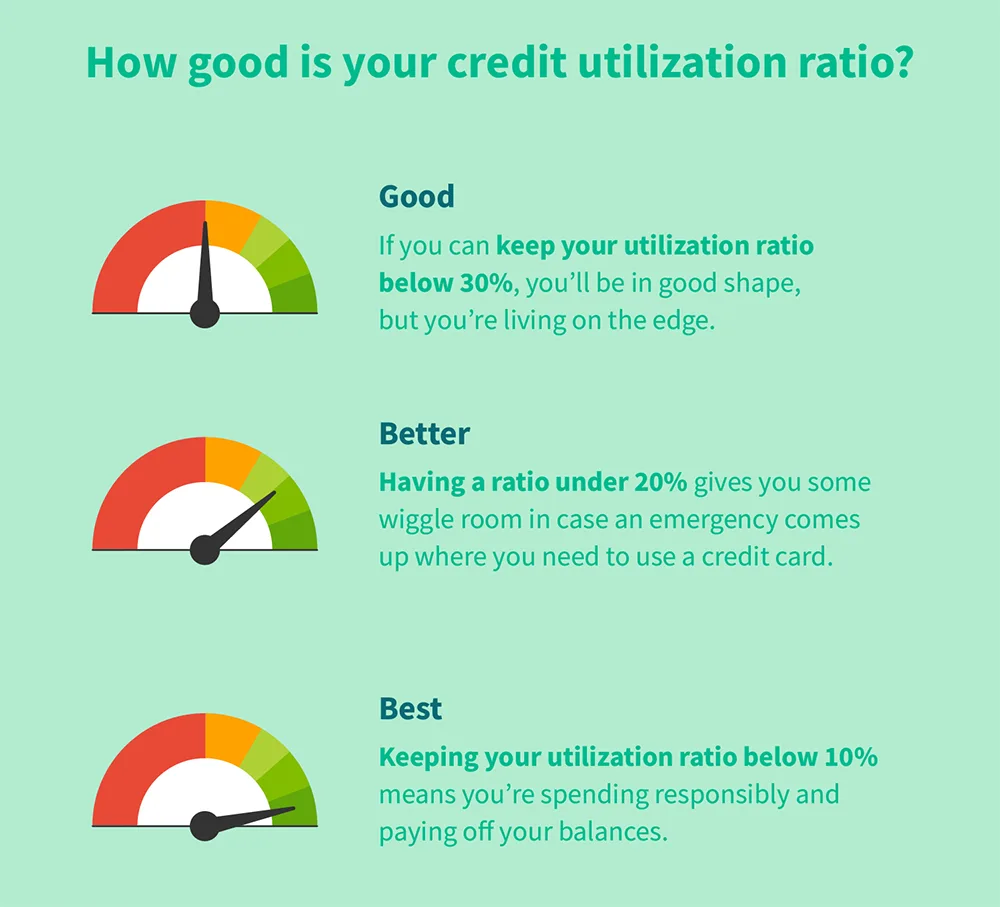

The Ideal Credit Utilization Ratio

Financial specialists usually advise people to keep their credit utilization at or below 30%. This mark is especially important because if you go over it, the negative effect will start to show up in your credit score in fact. Hence, if you get your credit utilization below 10% it is even better for increasing your score over time. For those looking to quickly improve their credit scores, consider exploring fast credit repair in 30 days.

Why Does Credit Utilization Matter?

Credit utilization is important because it demonstrates how responsibly you use your credit. A high ratio is a clear symptom of financial pressure, showing that you may depend on credit to meet all essential expenses. With this view in mind, it can make borrowing from banks an even less attractive option for you- because they’ll now worry less about whether or not their loans are going to work out. By extension, it will be harder as well to successfully apply for new credit cards or loans.

Why Does Higher Credit Utilization Decrease Your Credit Score?

The question, why does higher credit utilization decrease your credit score, is critical to understanding the dynamics of credit management. Credit scoring models, such as FICO and VantageScore, use credit utilization as one of the primary factors in calculating your score. Here’s how higher utilization negatively impacts your creditworthiness:

1. Increased Financial Risk

Lenders see you as a higher risk when you use a lot of your available credit. If you are already using a lot of your available credit, they may think that you have too much debt in relation to income. This perceived heightened danger is reflected in your credit score. The higher your use of credit and the more your credit score can drop, shows lenders that you might be unable to handle debts.

2. Limited Room for Emergency Borrowing

High credit utilization means you have little available credit left. If an emergency arises and you need to borrow money, you may not have enough credit available to cover the cost. This lack of flexibility can make you appear less creditworthy, further decreasing your score. Additionally, your ability to secure favorable rental terms may be affected if you’re asked for a move in fee vs security deposit when renting a property.

3. Impact on Creditworthiness Over Time

If credit use is consistently high then this will have a constant effect on the credit score, as rates of interest (notch point), balances and paying methods change. As long as your heavy balances exceed 30% of available credit for some time, this, in turn, is reflected by your score becoming an increasingly likely one to show ‘PAYMENTS LATE’. Nevertheless, just having high utilization-even when payments are always made on time- has its detrimental effect: gradually losing points from finally paying back your debts bears this out.

4. Negative Impact on Credit History

It provides information on your unpaid balances and the length of time they are kept so that other lenders can make decisions about whether or not go on offering credit in some form. When the numbers stay high for a long time, this too becomes part of your credit history and future chances for raising that score are much diminished. Lenders take them into consideration in determining whether making loans at all and will determine later terms of credit if you are offered a loan at all.

How to Manage Credit Utilization and Improve Your Score

Now that we understand why higher credit utilization decreases your credit score, let’s explore some practical ways to manage your credit utilization and improve your credit score.

1. Pay Down Balances Early

Another easy way to reduce your utilization is simply to pay off some credit card balances early. By keeping balances low, you demonstrate to potential lenders that you are able to manage your credit responsibly. By habitually settling your balance before each bill cycle, you can reduce your utilization rate over time. This increases your score. Additionally, this is an important strategy to consider if you’re looking to repair your credit score quickly.

2. Increase Your Credit Limits

If possible, you should ask your credit card issuer to raise your credit limit. However counterintuitive it might seem, increasing the total credit available and not actually running up charges can actually lower your credit utilization ratio. For example, if your credit limit is $5,000 and you have $1,500 on that card then 30% of it has been used. But when the ceiling goes up to $10,000 or even higher–now your revolving debts are only 15% as big. That looks much better in comparison.

3. Spread Balances Across Multiple Cards

If you have balances on more than one card, it’s best to pay them off separately. This way you can avoid a single max out of cards, which will be very damaging for your score.

4. Make Multiple Payments Throughout the Month

Instead of making one large payment every month, consider making more frequent smaller payments throughout the month. This strategy will keep your usage rate low–and periodic statement closing dates from sending it (and therefore your scores) soaring.

5. Set Up Alerts and Reminders

Set up balance alerts or reminders with your credit card issuer to keep an eye on how much credit you’re using. These tools will tell you when you’re getting close to or exceed a certain utilization threshold, letting you make changes before it begins to affect your credit score.

How Long Does It Take for Credit Utilization to Affect Your Credit Score?

Credit utilization can start to affect your credit score immediately. As soon as your credit card issuer reports the amount and limit of your balance to the credit bureaus, the change in–or maintenance of–your utilization ratio shows up on your score. On the other hand, if you’ve just lowered utilization, then over one billing cycle and into the next must pass before improvements work their way through.

The Role of Time in Credit Score Recovery

While the present tense of use can drag down your score quickly, the recovery of that score, of course, takes time. Paying down balances and keeping your utilization level consistent and decent for several months will gradually bring up your score. Also, the older these high-utilization eras become in your credit history, the milder an impact they will have as stars are deducted from future payments for secondary unsecured loans. If you’re looking to dive deeper into managing your credit utilization, visit Experian’s guide to credit utilization to explore in-depth strategies and expert advice.

The Broader Impact of High Credit Utilization

Understanding why higher credit utilization depresses your credit score is an essential part of managing your overall financial health. In addition to lowering your credit score, high utilization is like a ripple effect on various aspects of your financial life:

1. Difficulty Securing Loans

When your credit score is low due to high utilization, lenders may be less willing to approve you for loans, such as personal loans or auto financing. Even if you are approved, the terms may not be as favorable, and you could end up with higher interest rates or fees. If you’re planning to rent a property, your credit score may also determine how much deposit is required for an apartment.

2. Higher Insurance Premiums

Sometimes insurance companies use credit scores as a factor to determine how much you will be charged for insurance premiums due to the higher risk involved in lending – though regulation now makes this almost impossible. High utilization may mean that an individual has a lower credit score than others and thus faces higher premiums on such insurance policies as auto or homeowner’s insurance.

3. Limited Access to Credit Cards with Better Terms

In the event you have a lower credit score and do not qualify for these more favorable terms available to men at our best, like low-interest rates, cash rebates or prizes – then high utilization only makes it harder. This may push you farther into debt.

Conclusion

So, why does higher credit utilization decrease your credit score? It boils down to how credit scoring models assess risk. The more of your available credit you use, the more financial stress you signal to lenders, resulting in a lower credit score. By understanding how credit utilization works and taking steps to manage it, you can protect your credit score and ensure access to the best possible financial products.

If you find yourself struggling with high credit utilization, consider paying down balances early, increasing credit limits, and making multiple payments throughout the month. By staying on top of your credit utilization, you can maintain a healthy credit score and secure better financial opportunities in the future.

FAQs

How much should my credit utilization be?

Experts recommend keeping your credit utilization below 30%, with an ideal range being under 10% for optimal credit health.

How often do credit card companies report utilization?

Credit card companies typically report your balance and credit limit to credit bureaus once per month, usually after the statement closing date.

Can closing a credit card increase utilization?

Yes, closing a credit card can reduce your available credit, which may increase your utilization ratio and negatively impact your score.

Will paying off my entire balance improve my credit score?

Yes, paying off your entire balance will reduce your utilization and likely improve your credit score, especially if you maintain low balances going forward.

How quickly can I improve my credit score by lowering utilization?

You can see improvements as soon as the next billing cycle, but it may take several months of consistently low utilization for significant score recovery.

Does carrying a small balance help my credit score?

Carrying a small balance may not help your score and could even slightly lower it due to interest charges. It’s generally better to pay off your balance in full.