How Long Does a Hard Inquiry Affect Your Credit Score?

When it comes to managing personal finance, understanding your credit score is crucial. One common question many individuals have is, “How long does a hard inquiry affect your credit score?” Hard inquiries can play a significant role in determining your creditworthiness, impacting your ability to secure loans and credit cards. This article will explore the concept of hard inquiries, their impact on credit scores, how long they last, and strategies for managing their effects effectively.

How Long Does a Hard Inquiry Affect Your Credit Score?

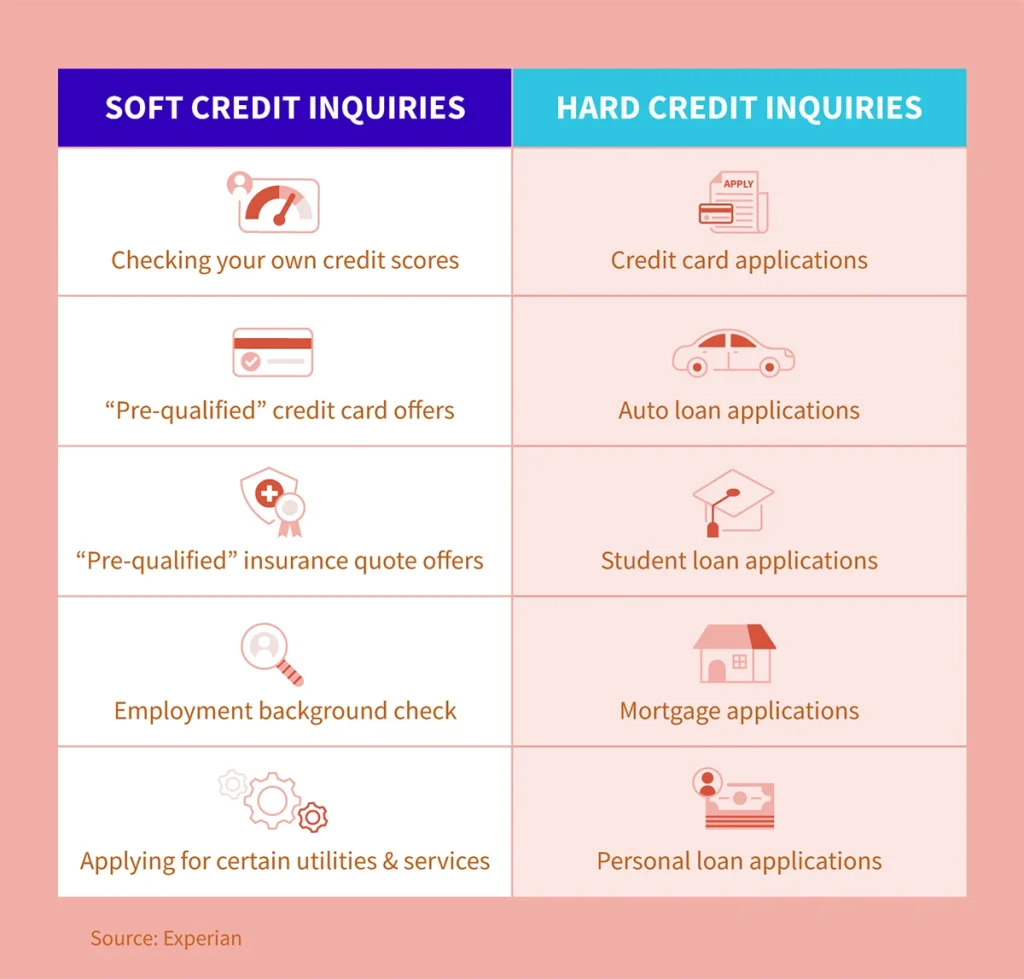

A hard inquiry or hard pull is where a lender checks your credit report as part of their evaluation process for a loan or credit application. In your credit file, lenders look at how well you’ve managed debt before, so they use this process to gauge whether it would be risky to give you any more money. Unlike soft inquiries, such as ones made when you’re checking your own credit report or if a firm offers you an offer that’s contingent on penultimate credit checks and background screening, hard inquiries are noted in your credit file, and this can indeed scale back some of the points which were added to your credit score.

How Do Hard Inquiries Affect Your Credit Score?

Hard inquiries can lead to a temporary drop in your credit score, but the degree of impact varies based on several factors:

- Hard Inquiries Quantity: If you have several hard inquiries accrued over a short period, then lenders may interpret this as an indicator of financial problems. And thus, your score can decline more significantly. Normally, one hard inquiry might mean that your score falls as few as 5-10 points at most. But for lots and lots of inquiries the effect snowballs before you know it into something much bigger.

- Credit History: Also affecting how much your score might go down is your overall credit history. If you’ve had a long good standing and a fairly high numeric credit score, even one hard inquiry won’t do much to it. On the other hand, if all those years are relatively modern and new, its impact grows massively.

- Credit Score Range: The first impact of a hard inquiry will be greater for those with higher credit scores. For example, a person above 700 points might see only a small drop; one under 600 could witness significantly larger falls in marks.

Understanding how TransUnion Credit Score Ranges work can help provide insight into how hard inquiries might impact your credit. The score ranges can give you a clearer picture of where you stand and how much of an effect each inquiry may have.

Duration of Impact

The effects of a hard inquiry on your credit score are generally temporary, lasting around six months to a year before diminishing significantly. Here’s a more detailed timeline:

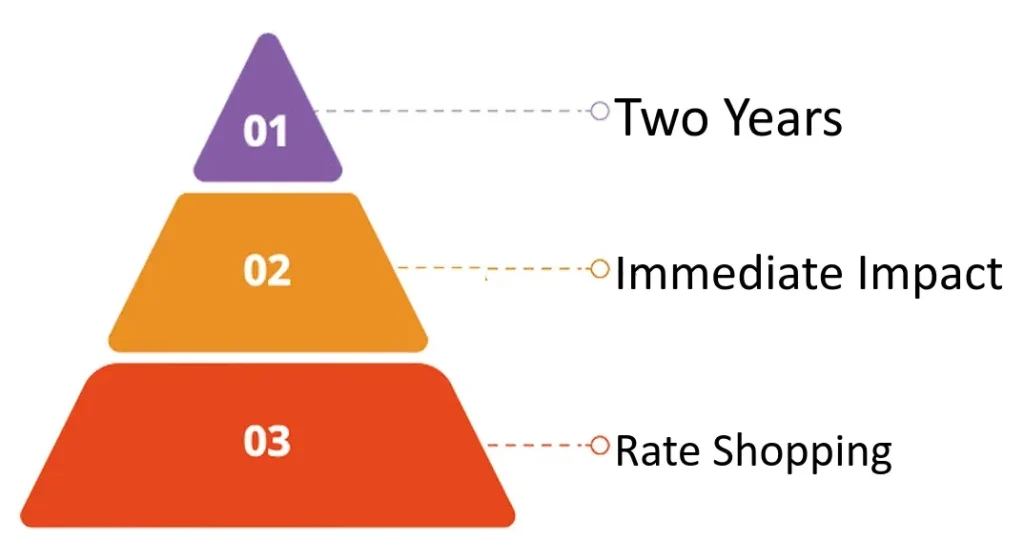

- Right away: When an inquiry occurs, you may drop to the immediate impact on your credit score. This decrease is usually no more than a few points, but remember that it’s temporary * (. It refs typically not less than one month).

- 6 Months Later: After 6 months, the impact from a hard inquiry starts to diminish noticeably. Many lenders stop caring about more mature checks, especially if your credit behavior remains good during this period.

- After One Year: By the time an inquiry hits 12 months old, it generally has little or no effect on your credit score. At this stage, lenders often look at how you’ve been handling credit as a whole and not just any earlier inquiries.

- After Two Years: Hard inquiries remain on file for two years. After this period has expired, the inquiry will disappear from your report automatically and not affect your score any longer.

Factors That Influence Credit Score Changes

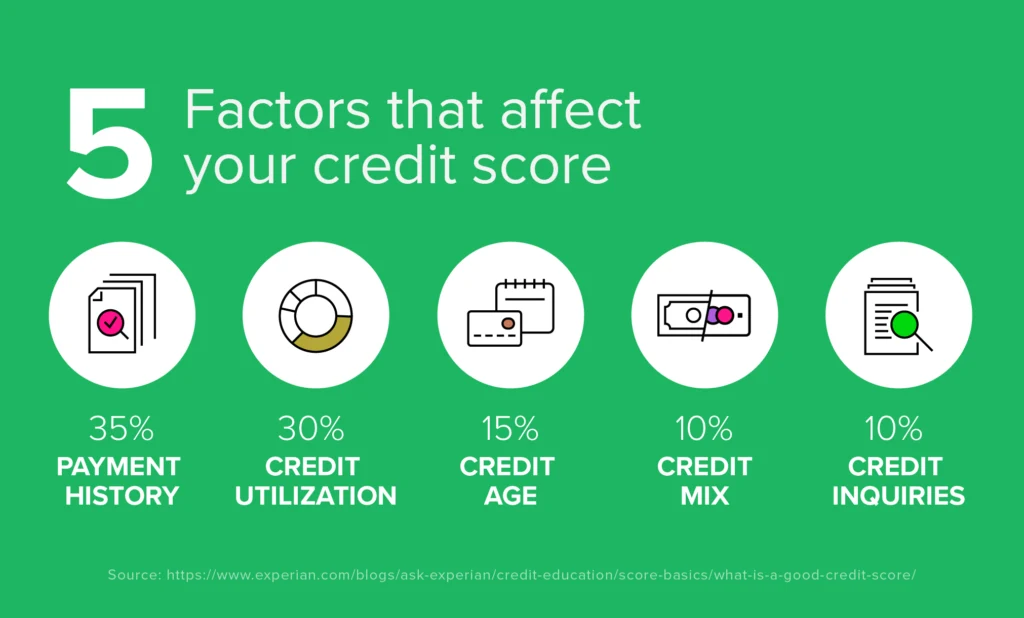

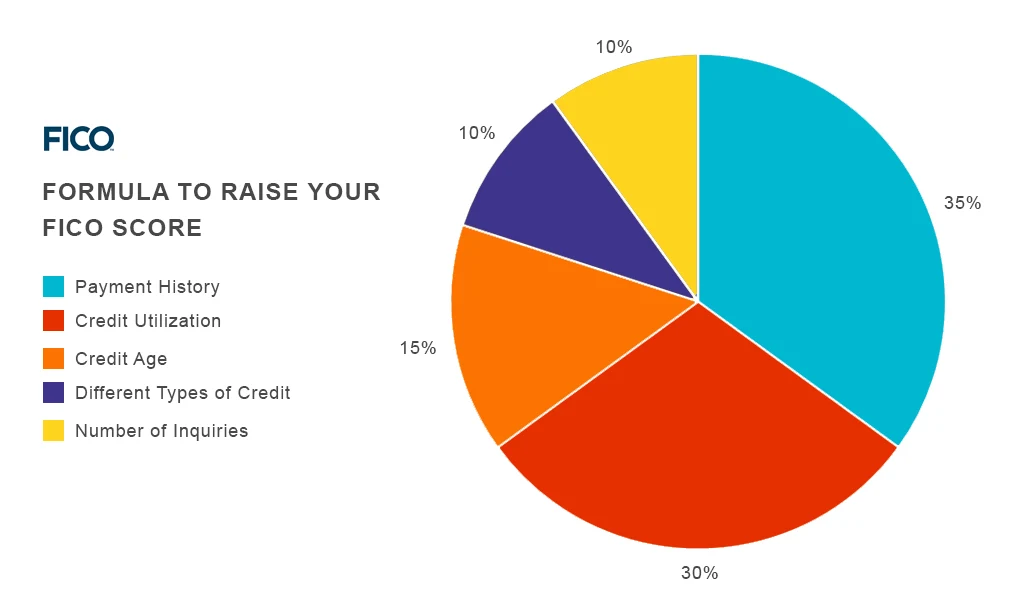

While hard inquiries are an essential factor in credit scoring, they are just one of many components that lenders consider. The FICO scoring model and other credit scoring systems evaluate several factors:

- 35% Payment History: This is the largest factor which influences your credit score. Consistent on-time payments can help rectify the problems resulting from hard inquiries.

- CREDIT Utilization (30%): This is the ratio of your credit card balances to the total credit you are allowed. It is generally recommended that you aim for a ratio under 30%.

- The LENGTH’ of Credit History (15%): The longer you have made credit payments, the higher your score will be. Opening new accounts may lower the average age of your accounts which might cause a short-term drop in score.

- TYPES of Credit (10%): The more different credit types (revolving likes credit cards and installment such as mortgages) on your records, the better it looks for scores.

- NEW Credit (10%): This category includes the number of recent accounts opened and hard inquiries. Lenders expect to see that you are not taking on too much new credit at one time, which could mean instability.

For more information about how factors like credit utilization can impact your score, check out why does higher credit utilization decrease your credit score for a deeper understanding.

The Impact of Hard Inquiries on Loan Approval

Even though hard inquiries can lower credit scores, you must understand their significance when it comes to loan approval. Lenders want to make sure that borrowers are responsible and can afford to repay their debts. Such’. If a credit report term often seen the sites it indicates that lenders will view you as a smaller risk and so you’ll pay higher interest rates or face altogether rejection for this line of credit.

How to Minimize the Impact of Hard Inquiries

If you are concerned about how hard inquiries may affect your credit score, there are several strategies you can employ to minimize their impact:

- Limit Applications: If you want to reduce the number of tough questions to your credit report, then one of the most effective methods is to limit your applications for loans. Only borrow when it really necessary and ask yourself whether or not you really need another account.

- Shopping Around for the Best Rate: If you shop for a loan, (like a mortgage or car loan), try and make all applications within a very short period of time–often 30 days! Many credit scores treat such applications in this way as cumulative and so will minimize the ultimate impact on your score.

- Make Sure Your Credit Is Accurate: Checking your credit report regularly will enable you to spot any changes and errors more swiftly. Every year, each of the three major credit reporting agencies (Equifax, Experian, and TransUnion) will provide one free credit report at AnnualCreditReport.com

- Develop Good Credit Habits: Setting up a monthly payment schedule, reducing outstanding debts and maintaining a minimal proportion of available funds used in the form of credit all have their benefits over time. Being diligently observed, these habits can go a long way towards limiting the negative impact of hard inquiries on your record.

- Use Prequalification Tools: Many lenders offer pre-qualification tools that allow you to establish your qualifications without affecting your credit score. Usually these tools involve soft inquiries, which do not have any impact on your score.

- Apply for credit before you want to apply for credit: The months before you expect to apply for a major loan such as a mortgage are not the time to be bench pressing and squatting 600 or 700 pounds. This strategy will keep your credit profile looking stable when you apply for the big loan.

What to Do After a Hard Inquiry

After a hard inquiry has been made, it is essential to take proactive steps to maintain or improve your credit score:

- Review Your Credit Report: After a hard hit to one’s rating, it’s a good idea to check over your credit report, making sure that all the information on it is accurate. If you find any discrepancies, get in touch with the credit bureau immediately.

- Continue Making On-Time Payments: Paying bills and other debts on time is the most important factor in building good credit. By keeping this up, you can offset some of the harm done by hard hits from SA’s.

- Limit New Credit Applications: Try to refrain from applying for new lines of credit immediately following a hard hit. Give your score the time it needs in order to rebound before going in search of additional credit.

- Be Patient: Keep in mind that hard hits on your rating are one-time occurrences. With time and new positive financial habits, your score should recover and may even improve.

Long-Term Strategies for Credit Health

To maintain a healthy credit score in the long run, consider implementing the following strategies:

- Establish a Budget: Create a monthly budget to help manage your expenses and avoid overspending. This practice can help you maintain a low credit utilization ratio and ensure you can make timely payments.

- Diversify Your Credit: While you should not open accounts you do not need, having a mix of credit types (such as credit cards and installment loans) can positively impact your score.

- Set Up Alerts: Many banks and credit card issuers offer alerts for upcoming payments and account changes. Utilize these features to stay informed and avoid missed payments.

- Educate Yourself About Credit: Understanding how credit works can empower you to make informed decisions. Read books, attend workshops, or take online courses about personal finance and credit management.

- Consider Credit Counseling: If you’re struggling with debt or unsure about your credit situation, consider seeking help from a certified credit counselor. They can provide personalized advice and resources to improve your credit health.

Suppose you’re looking to fix up a property. In that case, understanding the financial aspects of fixing up rental property is essential to maintaining good credit and minimizing debt, whether for yourself or as a rental investment.

Conclusion

They perform a necessary function in the credit application process; while they can temporarily damp your score, knowing their effects can help you get on with your finances effectively. For example, by being mindful of when and how often you apply for credit–as well as monitoring your credit report, and practicing good habits that build up positive entries in your credit history–you will have fewer hard inquiries to offset against future efforts at raising a healthy credit score. Additionally, taking advantage of resources like how to get a repossession off your credit and learning about rules for renting a room in your house can help you navigate both personal and rental finances more effectively.

Your credit rating is influenced by many factors which work together in concert, and hard inquiries are simply one facet. By taking charge of your finances, doing everything to boost balance, and learning from mistakes you have made in order to go forward in a calculated and successful way for example.Car Loan, When you want it to be Suggestions for you, Prepared Whether you ‘re Applying for a mortgage–you ‘d better know the ins and outs of hard inquiries in order to make your next credit decisions even more precise.